Retirement Income and Legacy Planning for Gen X

For decades, Gen X was taught to think about retirement in one narrow way: put money into a 401(k), hope the market cooperates, and eventually start drawing it down.

That is accumulation thinking.

At some point, retirement planning has to move from accumulation to architecture.

The question is no longer just, “How much did I save?”

The better question is how to turn what you saved into income you cannot outlive, while still building something meaningful for the next generation.

Retirement Planning Has to Move Beyond Accumulation

Accumulation matters.

You need the years of saving, investing, contributing, and compounding. But accumulation is not the whole retirement plan.

It is the raw material.

At some point, the planning question changes.

How will the money create income?

How much income needs to be predictable?

Which assets should remain invested?

Which assets should be protected from unnecessary risk?

What happens to the money after both spouses are gone?

How much of the estate is exposed to taxes, delays, confusion, or poor coordination?

This is where retirement income and legacy planning becomes different from basic retirement savings.

A 401(k), IRA, annuity, life insurance trust, estate plan, and tax strategy should not operate like separate decisions made in separate rooms.

They should be designed as part of the same structure.

Who This Kind of Strategy Is Actually For

This kind of planning is usually relevant to a specific stage.

It is for households that already have enough saved to cover their own retirement income needs and are now asking what happens to the rest.

If you are still building your retirement number, this strategy is probably not the priority yet.

Your focus may still need to be contribution rate, debt reduction, tax planning, investment allocation, business cash flow, or basic retirement readiness.

But if you are past that point and starting to think about estate exposure, tax consequences, income reliability, and what your children or heirs may inherit, the structure becomes worth understanding.

This is not about chasing a clever financial product.

It is about asking whether your retirement assets are designed to support income, protection, and legacy at the same time.

A Note Before Looking at the Illustration

I am a licensed annuities agent, and the illustration below reflects the kind of strategy I build for clients.

I am walking through it because the design is worth understanding, not because it is the right move for everyone.

Annuities and irrevocable trusts are specialized, largely permanent decisions. Anyone considering one should work directly with their own advisor and estate attorney before acting, whether that is with me or someone else.

The numbers below are illustrative.

The design is the point.

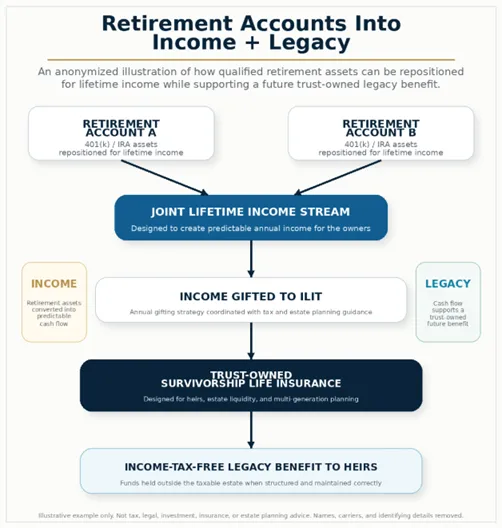

How a Retirement Account Can Become an Income Engine

In this hypothetical example, a couple starts with $350,000 combined across two 401(k) accounts.

Instead of leaving that balance exposed only to market performance and withdrawal decisions, the funds are repositioned to create an annual income stream backed by an insurance carrier.

In this illustration, the two 401(k) accounts are converted into joint-income life-pay annuities, producing a combined annual income stream of $241,373.

That income is then used as part of a larger legacy strategy involving an irrevocable life insurance trust, or ILIT.

Again, the numbers are illustrative.

The design is the point.

A retirement account can do more than sit in the market and wait to be drawn down.

Structured deliberately, it can become the engine that funds income, supports estate planning, and creates a legacy benefit for heirs.

How the ILIT Fits Into the Legacy Strategy

In this illustration, the annuity income funds a survivorship life insurance policy inside the irrevocable life insurance trust.

Upon the second death, the death benefit is paid to the trust.

From there, the trust can be used for estate taxes, family benefit, and future generations.

The illustration shows a $15 million death benefit paid to the ILIT after both grantors have passed.

Because the trust owns the policy rather than the individual, the death benefit may pass to heirs income tax-free and outside the taxable estate, depending on how the strategy is designed and maintained.

That last part matters.

The trust has to be structured properly.

The policy has to be owned properly.

The estate plan has to be coordinated properly.

The tax strategy has to be reviewed by the right professionals.

This is not a casual move.

It is a coordinated planning strategy.

The Numbers Are Not Magic. The Structure Is the Point.

The illustration is intentionally dramatic:

$350,000 starting point.

$241,373 a year in lifetime income.

A $15 million legacy.

The gap between those numbers is not magic.

It is time, deferral, insurance design, underwriting, trust structure, and coordinated planning working together.

That is exactly why the design matters more than any single figure in the illustration.

The wrong takeaway would be, “Everyone should do this.”

The right takeaway is, “Retirement accounts can be structured with more intention than most people realize.”

A retirement account is not just an account statement.

It can be income.

It can be protection.

It can be part of an estate plan.

It can be part of a legacy strategy.

But only if the pieces are designed to work together.

The Shift Gen X Needs to Understand

Retirement planning is not only about having enough money to stop working.

It is about controlling what happens next.

Will your retirement accounts create predictable income?

Will they reduce pressure on your children?

Will they lose value to taxes, market timing, estate costs, or poor coordination?

Or are they structured to support your lifetime income and still leave something behind?

For Gen X, the clock is getting shorter.

Many are in peak earning years while also carrying aging parents, adult or teenage children, business risk, debt, and retirement accounts that may or may not be enough.

The response to that is not panic.

It is design.

Design means putting the right specialists in the room before decisions are forced by age, illness, taxes, market timing, or family crisis.

Most People Do Not Need More Scattered Accounts

Most people do not need more scattered investment accounts.

They need a coordinated plan.

A 401(k), IRA, annuity, life insurance trust, estate plan, and tax strategy should not live in five separate conversations with five separate people who never talk to each other.

That fragmentation is where problems start.

The investment advisor may be focused on portfolio performance.

The insurance agent may be focused on income or death benefit.

The estate attorney may be focused on documents.

The tax professional may be focused on current-year tax exposure.

Each piece may be technically correct and still fail to operate as a complete strategy.

For households where it fits, the right structure can turn retirement savings into both lifetime income and a legacy asset.

But that only happens when the plan is designed as a whole.

A Retirement Account Is Raw Material

A retirement account is not the finish line.

It is raw material.

What you build with it determines whether it becomes income, security, and legacy, or just another account statement your family has to untangle later.

For some households, the answer may be simple: keep saving, keep investing, reduce debt, and build a stronger retirement foundation.

For others, especially those with enough saved to cover income needs and a desire to leave a meaningful legacy, the next question is structure.

How will the assets create income?

How will they transfer?

How will taxes be handled?

How will heirs be protected?

How will the plan hold together when life no longer goes according to the spreadsheet?

That is the real work of retirement income and legacy planning.

Not just saving the money.

Building the structure that tells the money what to do.

Start with the Retirement Protection Profile. It can help you see whether your current plan is built for income, protection, legacy, or just accumulation.